Dakuku

A statement from China’s Politburo meeting this month confirmed the central government’s readiness to take expansionary fiscal policy into 2024. The caveat to this pro-growth stance is that any easing will be implemented. “At an appropriate pace” – In my view, against the backdrop of slowing growth, deflation, and strong geopolitical headwinds, there is hardly enough intervention. In this environment, stock picks should outperform broader stock indexes as different sectors are disproportionately affected. China’s high-tech sector is a key focus area for tech-focused ETFs such as Invesco’s China Technology ETF (NYSEARCA:CQQQ) is of particular interest given that the technology is an area of strategic importance and will need to receive significant political and financial support going forward. However, this needs to be balanced against the backdrop of sluggish consumption and external geopolitical headwinds (such as US semiconductor sanctions).

I We are positive about the risk/reward of major Chinese high-tech ADRs this year (see previous coverage on Baidu)Bidu) here and Tencent (OTCPK:TCEHY) here), the CQQQ rating tips the balance in the other direction. Even after this year’s downgrade, the ETF, which tracks onshore and offshore tech stocks, trades at a forward price-to-earnings ratio of 27.7 times and has a subpar ROE of 6.8%. This limits the upside from the bottoming out of the semiconductor cycle and secular growth from artificial intelligence, a theme that has so far been limited to a few Chinese beneficiaries. However, the fund remains exposed to a wide range of macro and geopolitical tail risks, as well as company-specific execution hurdles. Net, the risk/reward doesn’t seem ideal here.

Invesco China Technology ETF Overview – A relatively concentrated Chinese tech portfolio

The Invesco China Technology ETF tracks the performance (before expenses) of the FTSE China Incl A 25% Technology Capped Index, which is a basket of constituents of the FTSE China Index and FTSE China A Stock Connect Index, which fall under the “Information Technology” category. ) track. In total, the fund invests more than 90% of its assets in depository receipts (US and global) as well as Hong Kong and mainland exchanges (i.e., Shanghai and Shenzhen). The key differentiator here is sector-specific exposure to a wide range of Chinese listed companies, including names not accessible to US investors.

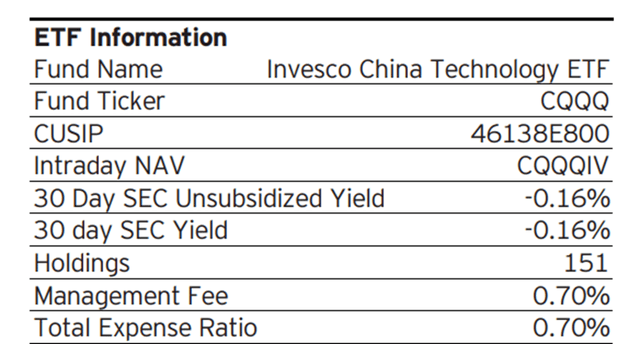

Despite the poor performance of Chinese stocks over the past few years, the ETF currently manages $676 million in assets, making it one of the largest and most liquid U.S.-listed Chinese tech ETFs. ing. The fund also has a relatively high expense ratio of around 0.7%, compared to major sector ETFs such as Global %, approximately 0.6% each.

invesco

Unlike its peers, CQQQ does not disclose its sub-sector composition in its monthly fact sheets. According to the latest semi-annual report, the largest allocation was to interactive media and services at 26.9%, followed by software (13.4%) and semiconductors and semiconductor equipment (13.0%). Rounding out the top five are hotels, restaurants and leisure (11.5%) and electronics, instruments and parts (10.3%). While other sub-sectors do not exceed the 10% threshold, it is still a fairly top-tier fund from a sector perspective, given that the top five sectors account for a significant portion of the total portfolio, around 75%. is.

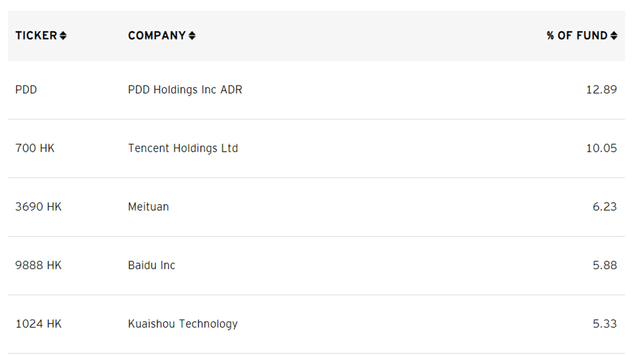

On the other hand, a breakdown of the fund’s individual stocks reveals that the portfolio is heavily weighted toward China’s biggest internet names. E-commerce company PDD Holdings (PDD) is currently the top holding with 12.9%, followed by tech conglomerate Tencent Holdings with 10.1%, consumer services platform Meituan (OTCPK:MPNGF) with 6.2%, and Baidu with 6.2%. It is 5.9%. CQQQ’s top four holdings are classic stocks that most other large-cap China ETFs tend to own, but the rest of the fund’s 154-stock portfolio includes optical lens maker Sunny Optical (OTCPK: SNPTF), Kingdee International Software Group (OTCPK:KGDEF), and A-shares such as Sanan Optoelectronics.

invesco

Given its concentration, this may be less suitable for more risk-averse investors compared to comparable funds such as CHIK and TCHI, which offer a less concentrated single stock profile. there is. On the flip side, these funds don’t have much influence from China’s heavily regulated “big tech” names, so investors will have to decide what kind of risk they’re most willing to accept.

Invesco China Technology ETF performance – dragged down by sharp decline in recent years

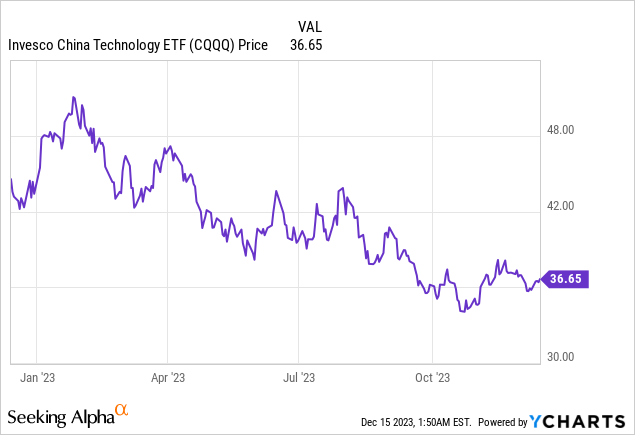

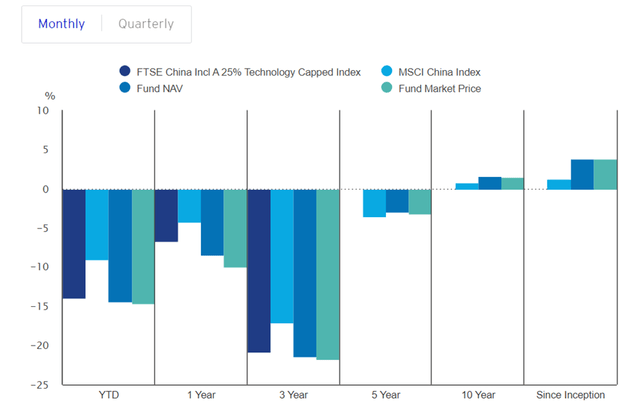

It’s been a disappointing year for CQQQ, with the ETF returning -14.4% year-to-date (-14.7% at market price), lower than MSCI China’s return of -9.0%. Over the past year, the fund has lagged a similarly broad China index tracker at -8.5% p.a., but the fund has slightly outperformed its leading peer CHIK (-9.3% p.a.) However, it fell short of the recently launched TCHI (-2.5% annualized rate). ). Meanwhile, over the past 10 years since its founding in 2009, annual total returns have remained positive (outperforming MSCI China) thanks to CQQQ’s post-2008 financial crisis gains.

invesco

The only other performance bright spot was the fund’s tracking error (adjusted for expenses) compared to the benchmark FTSE China Inc. A 25% Technology Capped Index, despite quarterly rebalancing. However, it remains at a narrow level. When it comes to CQQQ’s trailing distribution yield, the lowest 0.1% figure makes it clear that this is not a fund for income-oriented investors. We do not expect this pace of distributions to change anytime soon, as many of the fund’s holdings are still in growth mode.

Lucifer

Stock prices of Chinese tech companies soar

Investing in Chinese stocks has always been easier if you work with the government, but the technology sector has struggled in this regard in recent years. However, given the current macro and geopolitical context, the situation is changing. The administration’s increasingly pro-tech/private sector tone shows that interests are more aligned than ever. It also doesn’t hurt that the cyclical recovery of high-tech hardware and semiconductors, a key subsector component of CQQQ, is on hold.

However, details of this fund have not yet been revealed. Chinese technology companies remain exposed to significant macro and geopolitical risks, the latter of particular concern given the role of cutting-edge chips in the latest wave of technological innovation. In contrast, the market appears to be too optimistic on these issues, especially mainland-listed tech stocks, which is the main reason for CQQQ’s high forward P/E valuation in the low double digits. There is. Compared to the high bar, ROE needs to improve significantly from his current low-single-digit %, and so does revenue growth. Net Net, I don’t think taking on such a positive assumption is particularly convincing here. Instead, I would look for opportunities in the names of devastated individuals.

Source link